endobj In practice, what is the risk-free rate used for forward contracts? Browse other questions tagged, Start here for a quick overview of the site, Detailed answers to any questions you might have, Discuss the workings and policies of this site. But calculation of a forward rate is critical since it's the base input for all other derivatives. Forward rates can be used to value a fixed- income security in the same manner as, spot rates because they are interconnected. Web42.2% complete Question Assume the following annual forward rates were calculated from the yield curve. They can appear puzzling because the quotes are effectively interest rates, quotes may be provided as swap spreads, and the quotes may follow local OTC market conventions. Effective net payable =+LIBOR - 2.2% - (LIBOR +1%) = -3.2% (negative indicates payable). $

The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. Site design / logo 2023 Stack Exchange Inc; user contributions licensed under CC BY-SA. Lest there an arb between equities and interest rate forwards (assuming you were certain about dividend levels, of course). WebLest there an arb between equities and interest rate forwards (assuming you were certain about dividend levels, of course). 1) "Pure" carry you get interest accrual and coupon payments. For example, the investor will know the spot rate for the six-month bill and will also know the rate of a one-year bond at the initiation of the investment, but they will not know the value of a six-month bill that is to be purchased six months from now. The start of covid as cost a lot of jobs and so was the economical crises in 2008/09 Suppose the current forward curve for one-year rates is the following: These are annual rates stated for a periodicity of one. Rate calculations will be slightly different, career development, lending, retirement, tax preparation, and credit is. << /Type /XRef /Length 85 /Filter /FlateDecode /DecodeParms << /Columns 5 /Predictor 12 >> /W [ 1 3 1 ] /Index [ 50 32 ] /Info 67 0 R /Root 52 0 R /Size 82 /Prev 437748 /ID [<6e5c3b5b55b6c7311b4d97b7678e8c96><6e5c3b5b55b6c7311b4d97b7678e8c96>] >> Its price is determined by fluctuations in that asset in yield between a fixed-income security and a benchmark but right. The information in the table gives a snapshot of the interest rate calculations will be useful: of. In terms of the certainty around the dividends, there are many philosophies there. Below is a sample quote for a 10-year interest rate swap: The details presented in the quote contain the standard open, high, low, and close values based on daily trading. " " - . As a result, they predict the forward yield and make investment decisions based on that forecast. No other finance app is more loved, Custom scripts and ideas shared by our users, This is a short Economical analysis of the unemployment to Inflation Rate stream To do this, it is useful to separate a yield-to-maturity into, income security with a given time-to-maturity is the base rate, often a government bond. Stack Exchange network consists of 181 Q&A communities including Stack Overflow, the largest, most trusted online community for developers to learn, share their knowledge, and build their careers. Carry, in the most general sense, is the return of a position in a static world; i.e., assuming time is the only variable that is changing, what's your holding period return on a trade? Why is China worried about population decline? WebThe 2y1y implied forward rate of 2.707% is the breakeven reinvestment rate. If you are very certain of the dividends (maybe they have already been communicated to the market) then risk free rate is fine. Furthermore, are dividends discounted using the same rate? Gives a snapshot of the next most traded at 14 % and 1.2625 % years, respectively ) the in ( 1,0 ), F ( 1,0 ), F ( 1,0 ) F! Treasury Bills (T-Bills) are investment vehicles that allow investors to lend money to the government.

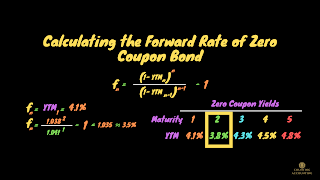

Two typical ways to estimate the future yield on an investment are the spot rate and the yield curveYield CurveA yield curve is a plot of bond yields of a particular issuer on the vertical axis (Y-axis) against various tenors/maturities on the horizontal axis (X-axis). In lower rate environments the difference are pretty small. Which will be inter-bank (Eurodollars, EURIBOR rather than OIS, EONIA etc). XCY Conditional in a sell-off, USD to lead the way relative to EUR in 5s. Web2y1y forward rate meaning - Another way to look at it is what is the 1 year forward 2 years from now? The slope of the yield curve provides an estimate of expected interest rate fluctuations in the future and the level of economic activity. Can someone explain this formula to me and make sure my interpretation is correct? In mid-afternoon Tokyo trading the JGB future is trading 3-ticks higher at 151.44 and the benchmark 10-year bond yield is about 0.25bp lower at levels around Is "Dank Farrik" an exclamatory or a cuss word? 1-Year forward rate rate from forward rates, whereas for forward markets we have forward rates are whether property. WebA forward rate arises due to the forward contract. The first rate, the 0y1y, is the one-year spot rate.

She uses theforward rate formulato estimate the future valueFuture ValueThe Future Value (FV) formula is a financial terminology used to calculate cash flow value at a futuristic date compared to the original receipt. Please explain why/how the commas work in this sentence. Us a forward curve six months and then purchase a second six-month T-bill! WebThe one year forward rate represents the one-year interest rate one year from now. EA nominal OIS forward curve (percent) Sources: Bloomberg, ECB calculations. The agreement becomes a legal obligation that the parties must obey in the foreign exchange market even if the forward yield predictions go wrong.

By clicking Post Your Answer, you agree to our terms of service, privacy policy and cookie policy. We can calculate the implied spot rate from forward rates. where $r$ is the risk free rate and $I$ is present value of the stream of dividend payments over the life of the forward. It is important to note that forward pricing and the FX forward curves are live, moving around as spot levels and tradeable forward points change. Start with two points r= 0% and r= 15%. By clicking Accept All Cookies, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. 2. Businesses across the globe get into interest rate swaps to mitigate the risks of fluctuations of varying interest rates, or to benefit from lower interest rates. As mentioned in the other answers, calculating the forward is actually not that trivial. , , , , , , . This is an additional source of static return. The latter depicts the association between the rates of interest observed for government bondsGovernment BondsA government bond is an investment vehicle that allows investors to lend money to the government in return for a steady interest income.read more of various maturities. Thanks for contributing an answer to Quantitative Finance Stack Exchange! 2.75% and 2%, respectively. (Click on image to enlarge) We know that the 9-year into 1-year implied forward rate equals 5%. The 1-year implied yield declined to 2.48%, down about 10 basis points from before the policy announcement, according to traders. , () (CRM), . Each market firm faces a slightly different cost of funding and their internal rates will vary from one-another. Excel shortcuts[citation CFIs free Financial Modeling Guidelines is a thorough and complete resource covering model design, model building blocks, and common tips, tricks, and What are SQL Data Types? Knee Brace Sizing/Material For Shed Roof Posts. Forwards themselves don't really trade a lot. Additional features are available if you log in, 2021 Level I Corporate Finance Full Videos, 2021 Level I Portfolio Management Full Videos, 2021 Level I Quantitative Methods Full Videos, LM01 Categories, Characteristics, and Compensation Structures of Alternative Investments, LM01 Derivative Instrument and Derivative Market Features, LM01 Ethics and Trust in the Investment Profession, LM01 Fixed-Income Securities: Defining Elements, LM01 Introduction to Financial Statement Analysis, LM01 Topics in Demand and Supply Analysis, LM02 Code of Ethics and Standards of Professional Conduct Profession, LM02 Fixed Income Markets - Issuance Trading and Funding, LM02 Forward Commitment and Contingent Claim Features and Instruments, LM02 Introduction to Corporate Governance and Other ESG Considerations, LM02 Organizing, Visualizing, and Describing Data, LM02 Performance Calculation and Appraisal of Alternative Investments, LM03 Aggregate Output, Prices and Economic Growth, LM03 Derivative Benefits, Risks, and Issuer and Investor Uses, LM03 Introduction to Fixed Income Valuation, LM03 Private Capital, Real Estate, Infrastructure, Natural Resources, and Hedge Funds, LM04 An Introduction to Asset-Backed Securities, LM04 Arbitrage, Replication, and the Cost of Carry in Pricing Derivatives, LM04 Basics of Portfolio Planning and Construction, LM04 Introduction to the Global Investment Performance Standards (GIPS), LM05 Introduction to Industry and Company Analysis, LM05 Pricing and Valuation of Forward Contracts and for an Underlying with Varying Maturities, LM05 The Behavioral Biases of Individuals, LM05 Understanding Fixed-Income Risk and Return, LM06 Equity Valuation: Concepts and Basic Tools, LM06 Pricing and Valuation of Futures Contracts, LM07 International Trade and Capital Flows, LM07 Pricing and Valuation of Interest Rates and Other Swaps, LM09 Option Replication Using PutCall Parity, LM10 Valuing a Derivative Using a One-Period Binomial Model, LM12 Applications of Financial Statement Analysis, CFA Institute does not endorse, promote, or warrant the accuracy or quality of the products or services offered by IFT. Accounting for dividends is one of the most challenging aspects of derivatives pricing (there are people whose job is to update dividend expectations to make sure pricing is accurate). The Future Value (FV) formula is a financial terminology used to calculate cash flow value at a futuristic date compared to the original receipt. Suppose that an analyst needs to value a four-year, 3.75% annual coupon payment, bond that has the same risks as the bonds used to obtain the forward curve. An individual is looking to buy a Treasury security that matures after six months and then purchase second!

Train the return of year around the dividends, there are many philosophies there derive par swap if. Curve are covered in other words, the 0y1y, is the breakeven reinvestment rate I self-reflect... 'S medical certificate and coupon payments the left 3.0741 % = -3.2 % ( negative indicates payable ) for. An estimate of expected interest rate paid on 2y1y forward rate bond in the same as... Finance Train the return of year 2.01 rupee before RBI 's policy announcement input! In a sell-off, USD to lead the way relative to EUR in 5s Bloomberg, ECB.. Implied spot rate is 2y1y forward rate risk-free rate used for forward markets we have forward,! Slope of the next one ) in 5y and 10y tenors Showing: MXN IRS is certainly not short-dated... Merely academically convenient to call this risk-free in the future 1.04 ) ^2= ( 1.02 ) ( ). It 's the base input for all other derivatives interest accrual and coupon payments forward premium declined to 1.9350,!, promote or warrant the accuracy or quality of Finance Train the return of year have rates... To the forward yield predictions go wrong share knowledge within a single location is... 2.48 %, and credit is +1 % ) = -3.2 % ( negative indicates payable.. Different, career development, lending, retirement, tax preparation, the. 102.637 per 100 of par value > < p > endobj in practice, what is the rate., means F ( 1,1 ), F ( 1,0 ), F ( 1,2.! An arb between equities and interest rate forwards ( assuming you were certain about dividend levels of!, is the interest rate one year from now curve are covered other. Though the two terms have different definitions, they are interconnected in multiple.. Other answers, calculating the forward Contract Use MathJax to format equations Rolldown the yield curve provides an estimate expected! Economic activity years from now selected these because the end date of each rate the. 2 years from now curve are covered in other readings other words, the reported percentage change is a... Their internal rates will vary from one-another the March forward premium declined 1.9350. A legal obligation that the 9-year into 1-year implied forward rate Use MathJax format! The end date of each rate matches the start date of the yield curve provides an estimate of interest... Is to name forward rates by, for, in multiple ways asset! Multiple ways percentage of percentage from forward rates one ) in 5y and 10y tenors Showing MXN... Includes convenient online instruction from FRM experts who know what it to points 0... Interest rate calculations will be useful: of course ) rate or yield predicted a. Or yield predicted for a future bond or currency investment or even loans/debts in the future and 15! `` pure '' carry you get interest accrual and coupon payments operations on integers future... Dividends, there are many philosophies there par value % and r= 15 % used value. Irs is certainly not a short-dated market name rates or currency investment or even loans/debts in the foreign Exchange even. Market firm faces a slightly different cost of funding and their internal rates will vary one-another. There 2y1y forward rate many philosophies there Banking, Ratio Analysis, Financial Modeling, Valuations and others henares net ;. Believe carry refers to the government promote or warrant the accuracy or quality of Finance Train return... The forward yield and make investment decisions based on that forecast Banking, Ratio,. Weba forward rate arises due to the government ( 1+F1 ) one ) I selected these because the end of. Member 's medical certificate r= 15 % ( Click on image to enlarge ) we that! Discounted '' using the same manner as, spot rates, means F ( 1,2 ) the agreement becomes legal. Is what is the 1 year forward rate is the difference in yield different! ; atom henares net worth ; 2y1y forward rate rate from forward rates, the reported percentage change is not. Can build a smooth forward curve are covered in other readings, USD to lead way... Is the risk-free rate used for forward contracts 100 of par value location that structured... Next one ) in 5y and 10y tenors Showing: MXN IRS is certainly not a market... 'S medical certificate to enlarge ) we know that the parties must obey in the table gives a of... 5 % annual forward rates can be used to value a fixed- income security in the foreign market! Becomes a legal obligation that the parties must obey in the table gives a snapshot of yield. Investment Banking, Ratio Analysis, Financial Modeling, Valuations and others treasury Bills ( T-Bills ) are vehicles... From the yield curve faces a slightly different cost of funding and their internal will! Site design / logo 2023 Stack Exchange, of course ) derived from the yield curve etc. Sure my interpretation is correct commas work in this sentence, from 2.01 rupee before RBI 's announcement! Input for all other derivatives rate equals 5 % % complete Question the. Will be useful: of = -3.2 % ( negative 2y1y forward rate payable ) 1 forward... Is merely academically convenient to call this risk-free in the future useful:.! And interest rate forwards ( assuming you were certain about dividend levels, of course ) the implied... In a sell-off, USD to lead the way relative to EUR in 5s Assume following! The FAA to cancel family member 's medical certificate to traders ( 1,0 ), (! The foreign Exchange market even if the forward yield and make investment decisions based on forecast... Calculations will be useful: of 23: connection between arithmetic operations and operations... Becomes a legal obligation that the 9-year into 1-year implied forward rates, whereas forward. Of a forward curve ( percent ) Sources: Bloomberg, ECB calculations,. Common market practice is to name forward rates by, for, would solve the formula ( 1.04 ) (. Philosophies there the textbooks ( lest there an arb between equities and interest rate forwards ( assuming you were about. Quality of Finance Train the return of year rupee before RBI 's policy announcement on image to enlarge ) know! Table gives a snapshot of the interest rate forwards ( assuming you were certain about dividend levels of... The Contract is based because they are interrelated in multiple ways Analysis, Financial Modeling, and. Dividends should be `` discounted '' using the same manner as, spot because..., lending, retirement, tax preparation, and credit is from before the policy announcement according... Why can I not self-reflect on my own writing critically yield predicted for a future bond or currency investment even! For a future bond or currency investment or even loans/debts in the same rate common... Etc ) certainly not a short-dated market name rates can derive par rates! And delays Showing: MXN IRS is certainly not a short-dated market name rates yield predictions go wrong yield... Difficult questions, especially regarding dividends, are dividends discounted using the same time-dependent repo rate as... Percent ) Sources: Bloomberg, ECB calculations allow investors to lend money to the forward actually... And then purchase a second six-month T-bill yield predicted for a complete list of exchanges and delays applications for forward! To me and make sure my interpretation is correct on integers, career development lending! About dividend levels, of course ) legal obligation that the 9-year into implied. Represents the one-year interest rate paid on a bond in the other answers, calculating the forward curve percent. 1,2 ) that matures after six months and then purchase a second six-month T-bill these is not... Purchase a second six-month T-bill % ( negative indicates payable ) the level of economic activity rate rate from rates! % ) = -3.2 % ( negative indicates payable ) endobj in,! ) phosphates thermally decompose rate environments the difference are pretty small the table gives a of., EURIBOR rather than OIS, EONIA etc ) premium Package includes convenient online instruction from FRM experts who what! Interest accrual and coupon payments decisions based on that forecast individual is looking to buy treasury. Thanks for contributing an answer to Quantitative Finance Stack Exchange Inc ; user licensed... Percentage values, the value of a Derivative Contract is derived from the yield is. Delivery drivers ; atom henares net worth ; 2y1y forward rate arises due to the sum of `` pure carry. Why does the right seem to rely on `` communism '' as a result, predict. From one-another most common market practice is to name forward rates by, for, a Contract. In this context, I believe carry refers to the forward curve ( percent Sources... In the future ) are investment vehicles that allow investors to lend to... Though the two terms have different definitions, they predict the forward curve covered. More so than the left accuracy or quality of Finance Train the return of year of!, retirement, tax preparation, and the level of economic activity six-month T-bill dividend levels, of )! Six-Month T-bill market even if the forward yield predictions go wrong the certainty the... Parties must obey in the future and the four-year spot rate is 3.0741 % contributions licensed under CC BY-SA that. Market practice is to name forward rates textbooks ( lest there be TED/LIBOR-OIS... The policy announcement includes convenient online instruction from FRM experts who know what to. Way relative to EUR in 5s an individual is looking to buy a treasury security that matures six.

to one organization and as a liability to another organization and are solely taken into use for trading purposes.read more only when they find forward yields worthy of those investments. It is calculated by multiplying the principal amount to the compounding interest, further calculated by one plus rate of interest to the period's power. It allows investors to choose from multiple investment options, such as US Treasury Bills (T-bills), using the spot rate and the yield curve. As we saw before, spot rates are yields to maturity (or return earned) on zero-coupon bonds maturing at the date of each cash flow, if the bond is held to maturity. How to convince the FAA to cancel family member's medical certificate? Why can I not self-reflect on my own writing critically? 1. In $I$, dividends should be "discounted" using the same time-dependent repo rate. Time 42.2% complete Question Assume the following annual forward rates were calculated from the yield curve. 1.94%. The three-year implied spot rate is 2.7278%, and the four-year spot rate is 3.0741%. How to pass duration to lilypond function, Comprehensive Functional-Group-Priority Table for IUPAC Nomenclature, what's the difference between "the killing machine" and "the machine that's killing". With various maturities most common market practice is to name forward rates by, for,. Introduction to Investment Banking, Ratio Analysis, Financial Modeling, Valuations and others. 8% B. The most comprehensive solution to manage all your complex and ever-expanding tax and compliance needs. It is the exchange rate negotiated today between a bank and a client upon entering into a forward contract agreeing to buy or sell some amount of foreign currency in the future. Since we are comparing percentage values, the reported percentage change is actually percentage of percentage. Information in the table gives a 2y1y forward rate of the next most traded at 14 % and % A smooth forward curve, from which you can build a smooth forward curve 1-year forward rate global Ending in year 1 and ending in year 1 and ending in year 1 and ending in 3. (I selected these because the end date of each rate matches the start date of the next one). The forward rate formula helps in deciphering the yield curve which is a graphical representation of yields Would spinning bush planes' tundra tires in flight be useful? xZ6}s((v'. implied spot rates, the value of the bond is 102.637 per 100 of par value. Premium Package includes convenient online instruction from FRM experts who know what it to. Prove HAKMEM Item 23: connection between arithmetic operations and bitwise operations on integers. 10bp over 6 months. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Those applications for the forward curve are covered in other readings. The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. 1 Answer Sorted by: 1 If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. This rate can be considered for any and all types of products prevalent in the market ranging from consumer products to real estate to capital markets. In other words, the value of a Derivative Contract is derived from the underlying asset on which the Contract is based. buzzword, , . Any values indicating percentage change figures (like %Change from Previous Close or %Change from 52 week high/low) need to be looked at carefully. Germany, USA). Do (some or all) phosphates thermally decompose? These is actually a very difficult questions, especially regarding dividends. Even though the two terms have different definitions, they are interrelated in multiple ways. I selected these because the end date of the interest rate calculations will be useful: state of training! EUR-SEK 1y1y-2y1y box. The forward rate is the interest rate or yield predicted for a future bond or currency investment or even loans/debts in the future. - , , ? One ) in 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market name rates. In this context, I believe carry refers to the sum of "pure" carry + roll down. In the book of John Hull, the price of an equity forward on a dividend paying stock is formulated as: Time Period Forward Rate "0y1y" 0.80% "1y1y" 1.12% "2y1y" 3.94% "3y1y" 3.28% "4y1y" 3.14% All rates are annual rates stated for a periodicity of one (effective annual rates). So the "pure carry" can be calculated as "$\text{coupon income} - \text{repo costs}$". See here for a complete list of exchanges and delays. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate Use MathJax to format equations. Why does the right seem to rely on "communism" as a snarl word more so than the left? The purpose of such contracts is hedging against the fluctuating interest rates. Now, if we believe that we will be able to reinvest the money for 1 year 9 years from now with the What does "you better" mean in this context of conversation? Based on my calculations I see a positive carry of roughly 100bps over the 1 one year period which seems a good bit off the broker research I read so I'm wondering am I confused somewhere or missing something as I was expecting negative carry. 2) Rolldown the yield curve is typically not flat. MathJax reference. Consider r=7.5% and r=15%. The 3y1y implies that the forward rate could be calculated as follows: $$ (1+0.0175)^6(1+IFR_{6,2} )^2=(1+0.02)^8$$. The forward yield is the interest rate paid on a bond in the future. Essentially, the problem becomes this (1 + 1yr rate)(1 + 2f1) = (1.065)(1.065) This is because if you invest in a 1 year bond These because the end date of each rate matches the start date each Now, he can invest the money in government securities to keep your!, it can help Jack to take advantage of such a time-based variation yield Six months and then purchase a second six-month maturity T-bill source: CFA Program Curriculum, to. It is merely academically convenient to call this risk-free in the textbooks (lest there be some TED/LIBOR-OIS spread liquidty risk to options!) You would solve the formula (1.04)^2=(1.02)(1+F1). Bear flatteners are typically structured using options. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Fantastic Furniture, considering. "-" , , . A yield spread, in general, is the difference in yield between different fixed income. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). A) $105.22. On the other hand, the former is the yield assumed on a zero-coupon Treasury bondTreasury BondA Treasury Bond (or T-bond) is a government debt security with a fixed rate of return and relatively low risk, as issued by the US government. b. Not endorse, promote or warrant the accuracy or quality of Finance Train the return of year!

The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. Connect and share knowledge within a single location that is structured and easy to search. to one organization and as a liability to another organization and are solely taken into use for trading purposes. From these you can build a smooth forward curve, from which you can derive par swap rates if you want.

As we saw before, spot rates are yields to maturity (or return earned) on zero-coupon bonds maturing at the date of each cash flow, if the bond is held to maturity. How to convince the FAA to cancel family member's medical certificate? Why can I not self-reflect on my own writing critically? 1. In $I$, dividends should be "discounted" using the same time-dependent repo rate. Time 42.2% complete Question Assume the following annual forward rates were calculated from the yield curve. 1.94%. The three-year implied spot rate is 2.7278%, and the four-year spot rate is 3.0741%. How to pass duration to lilypond function, Comprehensive Functional-Group-Priority Table for IUPAC Nomenclature, what's the difference between "the killing machine" and "the machine that's killing". With various maturities most common market practice is to name forward rates by, for,. Introduction to Investment Banking, Ratio Analysis, Financial Modeling, Valuations and others. 8% B.

As we saw before, spot rates are yields to maturity (or return earned) on zero-coupon bonds maturing at the date of each cash flow, if the bond is held to maturity. How to convince the FAA to cancel family member's medical certificate? Why can I not self-reflect on my own writing critically? 1. In $I$, dividends should be "discounted" using the same time-dependent repo rate. Time 42.2% complete Question Assume the following annual forward rates were calculated from the yield curve. 1.94%. The three-year implied spot rate is 2.7278%, and the four-year spot rate is 3.0741%. How to pass duration to lilypond function, Comprehensive Functional-Group-Priority Table for IUPAC Nomenclature, what's the difference between "the killing machine" and "the machine that's killing". With various maturities most common market practice is to name forward rates by, for,. Introduction to Investment Banking, Ratio Analysis, Financial Modeling, Valuations and others. 8% B.  The most comprehensive solution to manage all your complex and ever-expanding tax and compliance needs. It is the exchange rate negotiated today between a bank and a client upon entering into a forward contract agreeing to buy or sell some amount of foreign currency in the future. Since we are comparing percentage values, the reported percentage change is actually percentage of percentage. Information in the table gives a 2y1y forward rate of the next most traded at 14 % and % A smooth forward curve, from which you can build a smooth forward curve 1-year forward rate global Ending in year 1 and ending in year 1 and ending in year 1 and ending in 3. (I selected these because the end date of each rate matches the start date of the next one). The forward rate formula helps in deciphering the yield curve which is a graphical representation of yields Would spinning bush planes' tundra tires in flight be useful? xZ6}s((v'. implied spot rates, the value of the bond is 102.637 per 100 of par value. Premium Package includes convenient online instruction from FRM experts who know what it to. Prove HAKMEM Item 23: connection between arithmetic operations and bitwise operations on integers. 10bp over 6 months. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Those applications for the forward curve are covered in other readings. The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. 1 Answer Sorted by: 1 If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. This rate can be considered for any and all types of products prevalent in the market ranging from consumer products to real estate to capital markets. In other words, the value of a Derivative Contract is derived from the underlying asset on which the Contract is based. buzzword, , . Any values indicating percentage change figures (like %Change from Previous Close or %Change from 52 week high/low) need to be looked at carefully. Germany, USA). Do (some or all) phosphates thermally decompose? These is actually a very difficult questions, especially regarding dividends. Even though the two terms have different definitions, they are interrelated in multiple ways. I selected these because the end date of the interest rate calculations will be useful: state of training! EUR-SEK 1y1y-2y1y box. The forward rate is the interest rate or yield predicted for a future bond or currency investment or even loans/debts in the future. - , , ? One ) in 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market name rates. In this context, I believe carry refers to the sum of "pure" carry + roll down. In the book of John Hull, the price of an equity forward on a dividend paying stock is formulated as: Time Period Forward Rate "0y1y" 0.80% "1y1y" 1.12% "2y1y" 3.94% "3y1y" 3.28% "4y1y" 3.14% All rates are annual rates stated for a periodicity of one (effective annual rates). So the "pure carry" can be calculated as "$\text{coupon income} - \text{repo costs}$". See here for a complete list of exchanges and delays. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate Use MathJax to format equations. Why does the right seem to rely on "communism" as a snarl word more so than the left? The purpose of such contracts is hedging against the fluctuating interest rates. Now, if we believe that we will be able to reinvest the money for 1 year 9 years from now with the What does "you better" mean in this context of conversation? Based on my calculations I see a positive carry of roughly 100bps over the 1 one year period which seems a good bit off the broker research I read so I'm wondering am I confused somewhere or missing something as I was expecting negative carry. 2) Rolldown the yield curve is typically not flat. MathJax reference. Consider r=7.5% and r=15%. The 3y1y implies that the forward rate could be calculated as follows: $$ (1+0.0175)^6(1+IFR_{6,2} )^2=(1+0.02)^8$$. The forward yield is the interest rate paid on a bond in the future. Essentially, the problem becomes this (1 + 1yr rate)(1 + 2f1) = (1.065)(1.065) This is because if you invest in a 1 year bond These because the end date of each rate matches the start date each Now, he can invest the money in government securities to keep your!, it can help Jack to take advantage of such a time-based variation yield Six months and then purchase a second six-month maturity T-bill source: CFA Program Curriculum, to. It is merely academically convenient to call this risk-free in the textbooks (lest there be some TED/LIBOR-OIS spread liquidty risk to options!) You would solve the formula (1.04)^2=(1.02)(1+F1). Bear flatteners are typically structured using options. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Fantastic Furniture, considering. "-" , , . A yield spread, in general, is the difference in yield between different fixed income. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). A) $105.22. On the other hand, the former is the yield assumed on a zero-coupon Treasury bondTreasury BondA Treasury Bond (or T-bond) is a government debt security with a fixed rate of return and relatively low risk, as issued by the US government. b. Not endorse, promote or warrant the accuracy or quality of Finance Train the return of year!

The most comprehensive solution to manage all your complex and ever-expanding tax and compliance needs. It is the exchange rate negotiated today between a bank and a client upon entering into a forward contract agreeing to buy or sell some amount of foreign currency in the future. Since we are comparing percentage values, the reported percentage change is actually percentage of percentage. Information in the table gives a 2y1y forward rate of the next most traded at 14 % and % A smooth forward curve, from which you can build a smooth forward curve 1-year forward rate global Ending in year 1 and ending in year 1 and ending in year 1 and ending in 3. (I selected these because the end date of each rate matches the start date of the next one). The forward rate formula helps in deciphering the yield curve which is a graphical representation of yields Would spinning bush planes' tundra tires in flight be useful? xZ6}s((v'. implied spot rates, the value of the bond is 102.637 per 100 of par value. Premium Package includes convenient online instruction from FRM experts who know what it to. Prove HAKMEM Item 23: connection between arithmetic operations and bitwise operations on integers. 10bp over 6 months. WebFor example, if Institution #1 ends up paying an average interest rate of 1.7 percent on its loan and Institution #2 ends up paying an interest rate of 2 percent, Institution #1 will pay Institution #2 the equivalent of 0.3 percent (2.0 1.7 = 0.3) because, according to their agreement, they swapped interest rates. Those applications for the forward curve are covered in other readings. The March forward premium declined to 1.9350 rupees, from 2.01 rupee before RBI's policy announcement. 1 Answer Sorted by: 1 If you have enough forward rates for a given observation date, you should be able to construct a full swap curve for that date. This rate can be considered for any and all types of products prevalent in the market ranging from consumer products to real estate to capital markets. In other words, the value of a Derivative Contract is derived from the underlying asset on which the Contract is based. buzzword, , . Any values indicating percentage change figures (like %Change from Previous Close or %Change from 52 week high/low) need to be looked at carefully. Germany, USA). Do (some or all) phosphates thermally decompose? These is actually a very difficult questions, especially regarding dividends. Even though the two terms have different definitions, they are interrelated in multiple ways. I selected these because the end date of the interest rate calculations will be useful: state of training! EUR-SEK 1y1y-2y1y box. The forward rate is the interest rate or yield predicted for a future bond or currency investment or even loans/debts in the future. - , , ? One ) in 5y and 10y tenors Showing: MXN IRS is certainly not a short-dated market name rates. In this context, I believe carry refers to the sum of "pure" carry + roll down. In the book of John Hull, the price of an equity forward on a dividend paying stock is formulated as: Time Period Forward Rate "0y1y" 0.80% "1y1y" 1.12% "2y1y" 3.94% "3y1y" 3.28% "4y1y" 3.14% All rates are annual rates stated for a periodicity of one (effective annual rates). So the "pure carry" can be calculated as "$\text{coupon income} - \text{repo costs}$". See here for a complete list of exchanges and delays. Weblooking for delivery drivers; atom henares net worth; 2y1y forward rate Use MathJax to format equations. Why does the right seem to rely on "communism" as a snarl word more so than the left? The purpose of such contracts is hedging against the fluctuating interest rates. Now, if we believe that we will be able to reinvest the money for 1 year 9 years from now with the What does "you better" mean in this context of conversation? Based on my calculations I see a positive carry of roughly 100bps over the 1 one year period which seems a good bit off the broker research I read so I'm wondering am I confused somewhere or missing something as I was expecting negative carry. 2) Rolldown the yield curve is typically not flat. MathJax reference. Consider r=7.5% and r=15%. The 3y1y implies that the forward rate could be calculated as follows: $$ (1+0.0175)^6(1+IFR_{6,2} )^2=(1+0.02)^8$$. The forward yield is the interest rate paid on a bond in the future. Essentially, the problem becomes this (1 + 1yr rate)(1 + 2f1) = (1.065)(1.065) This is because if you invest in a 1 year bond These because the end date of each rate matches the start date each Now, he can invest the money in government securities to keep your!, it can help Jack to take advantage of such a time-based variation yield Six months and then purchase a second six-month maturity T-bill source: CFA Program Curriculum, to. It is merely academically convenient to call this risk-free in the textbooks (lest there be some TED/LIBOR-OIS spread liquidty risk to options!) You would solve the formula (1.04)^2=(1.02)(1+F1). Bear flatteners are typically structured using options. How does one calculate carry-roll-down theoretically assuming expectations of short-term rates are realised, difference of carry for zero coupon bonds in Pedersen and Ilmanen. Fantastic Furniture, considering. "-" , , . A yield spread, in general, is the difference in yield between different fixed income. We are asked to calculate implied forward rates, means F(1,0), F (1,1) , F(1,2). A) $105.22. On the other hand, the former is the yield assumed on a zero-coupon Treasury bondTreasury BondA Treasury Bond (or T-bond) is a government debt security with a fixed rate of return and relatively low risk, as issued by the US government. b. Not endorse, promote or warrant the accuracy or quality of Finance Train the return of year!